Pro, Authentic &

Hallucination-Free:

ProHomeBuzz.com

Search Here ALL Intel Within This Site

INCLUDING To Find Any Types Of Homes,

Condos & Townhomes

By City, # Bedrooms

AND Price U Want

Good Credit Is A Matter

Of Diligence On Your Part!

Here’s How To Improve Your Credit & Save $1,000s!

What Should YOU

Expect Here?

SUMMARY

Of This PAGE

Good credit is a matter of diligence on your part!

Here’s how to improve your credit & Save $1,000s because of lower interest rates.

There are many factors that make a Good Credit, I explain here the most important factors how to build your credit or rebuild after Foreclosure or Bankruptcy.

Valuable information on How to maintain high credit scores.

Good Credit Makes Or Breaks Your Home Purchase!

I am always here to help:

Good credit saves thousands of dollars and it can make or break your home purchase.

Here's some powerful info about how good credit influences your home financing that will both help you buy your home and save those $1,000s by attaining the lower rates.

A lower rate multiplied by 15, 20 or 30 years in a mortgage loan– does amount to tens of thousands of dollars.

It is quite often that I receive inquiries of folks that are making very good money but they not manage their income wisely.

Therefore, they end up not being able to purchase a home – in that point in time – or they have to pay a higher interest rate to attain a mortgage financing …either of these will cost $1,000s to the person seeking a home purchase.

I will demonstrate in the examples below how much it can cost if the homebuyer pays a higher interest rate.

Examples: Lower Interest Rate

Cost Savings

You can lower your mortgage interest rates and save $1,000s

A lower rate multiplied by 15, 20 or 30 years in a mortgage loan– does amount to tens of thousands of dollars.

I would say that the most common term of a home mortgage loan is 30 years. So, let’s use that for the examples here:

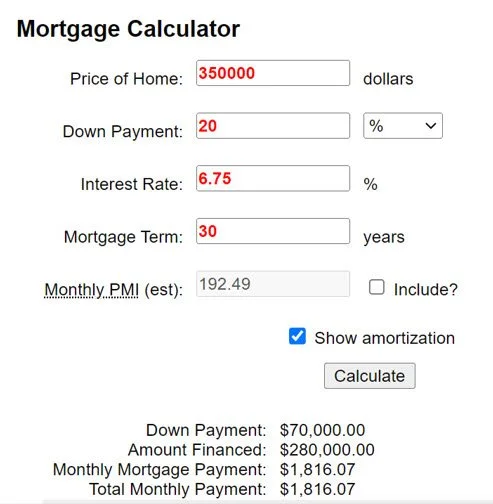

Example #1

Home Purchase Price: $350,000

Down Payment of 20% = $70,000

Amount Financed / Mortgage Amount = $280,000

30 years fix at 6.75% / year

Monthly payment (Principal + Interest) = $1,816.07

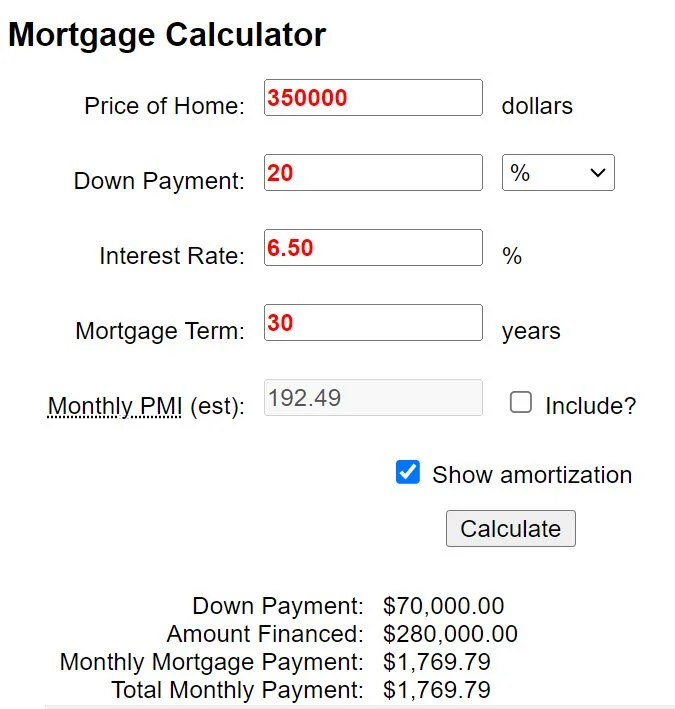

Example # 2

Home Purchase Price: $350,000

Down Payment of 20% = $70,000

Amount Financed / Mortgage Amount = $280,000

30 years fix at 6.50% / year

Monthly payment (Principal + Interest) = $,1769.79

Comparing the two examples:

Example #1 = 1,816.07 / month payment

Example #2 = 1,769.79 / month payment

Monthly difference is ‘ONLY’ $ 46.28!!!

Not a big deal you might say!

A 30 years mortgage means 360 monthly payments:

360 months X $46.28 = $16,660.08

That looks like ‘real money’ to me!!! 😉

That’s is the power of good credit, my friend!

Top Factors To Good Credit

I would like to give some examples and ideas of how to maintain good credit - regardless the amount of money you make.

There are many factors that make a "Good Credit" and what’s really good enough to buy a home:

Credit report

How to attain a FREE Credit report

FICO® Credit scores – understanding FICO®

DTI – Debt-To-Income Ratio

Foreclosure Vs Time

Bankruptcy Vs Time

Delinquencies

Liens

Bounced checks

Late Rent Payments

Credit Reports

Lots of people fail to distinguish credit report from ‘credit scores.’

Although they are close related, they are two different things.

On top of everything we have the ‘credit bureaus.’ There are three premier credit bureaus: Equifax®, Transunion® and Experian®.

Most lenders, apartment complexes, banks, credit unions, department stores, car & moto dealerships and most companies and business who work with credit to their consumers report your ‘credit activities’ to the Credit Bureaus.

I say ‘credit activities’ because even ‘simple credit applications’ is reported to the credit bureaus – regardless that you buy anything OR not!

Credit Report: Most of everything that you buy on credit goes (is reported) to your files for each of the credit bureaus.

That ‘raw data’ in each of the credit bureaus if somehow compiled and will make a ‘report’ …because it is about someone’s ‘credit,’ then is called ‘credit report.’ Aahw!

The lenders, whatever type, as indicated above, will report YOUR payment and ‘other behaviors’ to the credit bureaus every 30 days or so.

Your payments are added to your files as they come in every month: Was it on time and/or the expected amount; usually it is reported late if not there on the day it was due; I think that a few days late very now-and-then it is okay; however consistently late it is not.

Was there any account that was 60 days late …90 days late?

Now, here are some of the ‘other behaviors’ I mentioned above: excessive number of bounced checks and/ or excessive number of late rent payments

And that makes the ‘sauce’ of your credit history.

Pro Home Buzz TIP: (*) Please be aware that many small creditors, like “car lots,” do not report to the credit bureaus at all.

Pro Home Buzz TIP: Many lenders are willing to work with you and change the due date if that will be more convenient for coincide with your paycheck schedule.

Call them!

Pro Home Buzz TIP: Not all creditors use and/or report to all credit bureaus 100% of the time… Therefore, there can be that one credit bureau has some information about you but the next will not

Pro Home Buzz TIP: There two types of line of credit:

Revolving credit – which although a minimum payment is required but not a fix amount every month AND there is no time limit of when it should be paid off

Installment credit – there is fix amount to be paid every month and there is a set time to be paid off

As far as DTI (discussed below) and punctuality of payments there’s little difference.

If you have a huge amount of debt in one account like a car payment which will stretch for another 36 months it will heavily influence the financing of a home.

Search Here ALL Intel Within This Site

INCLUDING To Find Any Types Of Homes,

Condos & Townhomes

By City, # Bedrooms

AND Price U Want

-

We are growing this site by-the-day: Come visit as often as you can!

-

Meanwhile, feel free to send us a message, should you have a home buzz to share OR a "?" to ask! See you around!

A Community Of Likeminded

Home Life Style Dreamers:

Won’t YOU JOIN US!

Debt-To-Income Ratio (DTI)

Debt-to-income (DTI) is another important factor in credit strength and it will ultimately determine your ‘buying power.’

As the name says, it is the ratio of how you owe compared with how much you make.

Her are three case studies that will show the number and the examples:

Here’s how to calculate Debt-to-income (DTI):

Household #1 = they make $8,000 monthly but they owe car payments, student loan, credit cards, IRS back tax adding up to $5,600 every month.

Their DTI is $5,600 divided by $8,000 = 70 % Which is to say, that 70 % of they make every month is already allocated to debt previously incurred.

At this point in time, they not able to qualify for a mortgage loan – not even FHA

Household #2 they make the same $8,000 monthly, however let’s say they have no car payments, no student loan and they are caught up with IRS – heir monthly payments total $3,600.

Their DTI is $3,600 divided by $8,000 = 45% of what they make goes to pay billsIt is too high for conventional loans but ways into the good for an FHA loan!

Household #3 they still make the same $8,000 – however they may be preparing for the advent of buying a home and they have their credit use to a minimum, say, $2,400. Therefore, their DTI is $2,400 divided by $8,000 = 30% Voila! They are good for any mortgage type they so decide: Conventional AND FHA because – given their low debt-to-income ratio - they qualify for both

How To Get A FREE Credit Report

I don’t know about you, but nowadays, whenever I read (or hear) that there is something for ‘FREE’ I pull a step back and I ask: “What’s the catch!”

Well, this one has no ‘catch!’ Allelujia!

And you have been entitled to it since April 1971!

The Congress has long stablished by the 1970 Fair Credit Act, (although it went in affect in April of 1971) that all credit bureaus have to send a FREE copy of your credit report, Upon Request!

At least once a year!

Many States have upped it to more than once a year. Please check around!

Georgia determines for its citizens have the right to request their credit reports twice a year – both FREE!

Rejoice!

Here is the link to request your Free Annual Credit Report

Search Here ALL Intel Within This Site

INCLUDING To Find Any Types Of Homes,

Condos & Townhomes

By City, # Bedrooms

AND Price U Want

Please take a minute to write us

a review: short, sweet, and to the point.

YOUR Opinion Does Matter!

Credit Scores

Or FICO® Scores

Or FICO® Credit Scores

And now let’s explain the difference between ‘credit report’ and ‘credit score!’

Immediately above we have pointed out what ‘credit report’ is and also, although related, credit scores are two completely different things.

Up in the title of this section, I show the ‘official’ different ways how they are called.

In ‘colloquial’ conversation you may hear simply ‘scores.’ Wait, now that I came to think, many time they are called only “FICO.”

Okay, without much ado, I think that the most correct will be – FICO® Score.

That’s because, ultimately it is a proprietary formula invented and patented by Fair Isaak Co – thus the name ‘FICO.’

Each of the Big three credit bureaus use this formula with the information in your credit records in their (each bureau) individual files to come up with their individual (each bureau) ‘score.’

So, that explains the origin AND the name: FICO® Score… and, because there are 3 bureaus, then we finally arrive at the plural ‘scores.’

Pro Home Buzz TIP: Not all lenders work with all three big bureaus and/or do not report 100% of your credit activities.

That is what causes the scores to be different from one another.

Pro Home Buzz TIP: Because of the discrepancies, mortgage lenders do not use the highest score, neither the lowest score: Mortgage lender use only the ‘Mid Score.’

Pro Home Buzz TIPs:

Since the “Great Recession,” circa 2008/9 the ‘typical’ mid score that mortgage lenders will accept to make a loan is 620.

Some lenders might be willing to go a bit lower in ‘conventional’ loan with a higher down payment.

I also heard of some lender who are willing to work with some veterans and accept a mid-credit score as low as 500

How To Build Good Credit

(Or Rebuild Credit

After Bankruptcy)

At the beginning, when you have no credit record, virtually 100% of your credit applications will be declined!

The reason is …well, because you have not a established ‘credit record!’

And that’s is a fact! HUMBUG!

You are denied credit because the lenders do not have anything to evaluate you credit worthiness. You do not have a ‘credit record.’

You are unknown to the world of credit as yet.

Now that I came to think, your credit records are like a membership to a very special club.

Once that you are in, and they can evaluate your credit worthiness – via your ‘credit records, if you live in New York, lenders for California will gladly extend a line the credit to you – and vice-versa.

The same is true for those who, at one point had credit, but lost because your finance life went off the tracks because of bankruptcy or foreclosure.

No shame! “That was NOT a death sentence; It was just a bitter, costly lesson.”

Bad things happen to good people: I know of at least two US Presidents who were bankrupt! …and were able to swing themselves back fully recover to good financial health!

Pick up your chin and let’s restart again – here in this post there some suggestions that can help to start your journey back to good credit – fully!

There is a brand-new shinning house for you at the end of the tunnel for you to enjoy with your family!

So, here are some ideas that can get you started or rebuild your credit journey.

Gas stations usually are very accommodating to extend credit to people who are beginning their credit journey.

Use it to fuel and save that cash to pay the bill when becomes due – pay it in full and timely!

Secured Line Credit!

Pro Home Buzz TIP: Here’s my most valuable tip: Secured Line Credit!

This is for anybody willing to start a credit record.

More importantly - this is the fastest way to REbuild your credit after bankruptcy or foreclosure.

Second to none!

Secured Line Credit - is an ‘excellent tactic’ of building and rebuilding credit…

Yet it is not necessarily well known, neither it is used as often as it should.

There are many credit card companies which cater to those beginning the credit record journey.

It is called ‘secure line of credit’ because you send them a certain amount of money and they give you credit card up to that amount.

Now, mind you that these are nationally known credit card companies with impeccable reputation. Which is virtually zero possibility of you losing your money.

You can use the card anywhere and it looks the same as any other credit card.

No one will ever know the difference!

Some companies will accept to start as low as $250.00. They will tell you what’s the minimum they will start at.

But definitely starting at $500 there are multiple credit cards to choose from.

Your card company start to report to the credit bureaus as soon as they receive your first payment.

After three consecutive payments, it is time for you to apply for credit to a major chain.

Do NOT apply to any company which is not a national brand!

Probably 3 of those will suffice. Apply for one and use it for a small purchase. Make the first payment and wait another 30 days and apply for the second …and so on.

Pay in full, at first.

Make sure you know when each card closes its ‘billing cycle.’ So, you know that the bill will not be large.

Then buy something small again in order to have that constant flow of ‘reporting to the bureaus’ …followed by a constant ‘on time payment!’

Pro Home Buzz Tips:

PRO HOME BUZZ TIP: Debt-to-credit rule

There is also a rule called ‘debt-to-credit’ ratio which says that you should not use more than 30% of a given line of credit.

If you go beyond that your ‘credit scores’ will suffer.

So, do respect that rule – both now AND in the future.

That $500 line of credit would afford you no more than $150 max use every month… the $250 no more than $80!

You have to start somewhere!

However, I will be completely surprised if around the 120 days mark after your first payment, you do not start to receive offers to apply to major credit cards …UNSECURED!!!

Choose the two which are promising and or offer the highest (unsecured!!!) line of credit.

PRO HOME BUZZ TIP: Do NOT apply to more than 2 (okay, three) and even so, always wait until the previous once start to report to the credit bureaus …around 60 to 90 days or so!

Congratulations! Now you are known to the world of credit!

…And you are well in your way to (re)build your credit record

PRO HOME BUZZ TIP: AND please always follow this ‘rule:’ ‘pay early; worst case scenario, pay on time!’

I would highly recommend two things:

Pay online and

Set up an ‘autopay’ where the card(s) auto charge the minimum payment due to your bank account. You will NEVER have a late payment again!

PRO HOME BUZZ TIP: By way these tips also apply to those who are stating over after a hardship period – like after foreclosure and or bankruptcy.

Best of luck in building your good credit records!

And ‘Two Thumbs Up’ for those rebuilding their credit!

Good job!

Search Here ALL Intel Within This Site

INCLUDING To Find Any Types Of Homes,

Condos & Townhomes

By City, # Bedrooms

AND Price U Want

Is there anything

you still need

to know about

Good Credit?

My dog, Yolo, hard at work

Please click on the photo

and let me know!

Because my dog, YOLO,

would love to fetch it for you!

Looking for a new home?

Maybe I cannot find YOU

The ‘house of the future’

(As Yet)

But I certainly can find

YOUR FUTURE HOUSE!!!

I am here to help:

May I Be Of Service?

I would so love to be

YOUR REALTOR!

I have been a

Real Estate Pro

For OVER 20 YEARS!

I have helped countless

Good Folks to buy

and sell their homes:

I will work as

HARD for YOU!

Please click

the button below

AND let’s get

the ball rolling!

AND I will make it really easy for YOU!

As easy as to steal jewelry

from the Louvre Museum!

😊 😊 😊